The first year of a presidency often reveals whether a governing philosophy can survive contact with reality. Promises are plentiful on the campaign trail, but economic facts are unforgiving. Prices either fall or they do not. Wages either outpace inflation or they do not. Families either feel relief at the grocery store and the gas pump, or they do not. As President Donald J. Trump approaches the end of his first 11 months back in office, the verdict is increasingly clear. The inflationary damage inflicted by the prior administration is being repaired, methodically and measurably, and Americans are beginning to feel the difference.

To understand the significance of this moment, it is necessary to recall the scale of the problem President Trump inherited. Under the Biden administration, inflation averaged nearly 5% and peaked at 9.1%, the highest level in four decades. This was not an act of nature. It was the predictable consequence of an ideological commitment to mass deficit spending, aggressive regulatory expansion, and energy scarcity. When trillions of dollars are injected into an economy without corresponding growth in production, prices rise. When domestic energy production is constrained, transportation and heating costs rise. These are not controversial propositions. They are basic economic truths.

President Trump ran on a promise to reverse this damage, and his approach has been straightforward. Reduce inflation first, then allow wages and growth to do the rest of the work. Eleven months in, inflation in Trump’s second term has averaged roughly 2.7%. That figure matters not as a talking point but as a threshold. It marks the difference between households treading water and households regaining ground. Even more striking, Americans have experienced the first overall price decline since 2020. Core inflation, often regarded as the most reliable measure because it strips out volatility, is now lower than at any point during the last three years of the Biden administration.

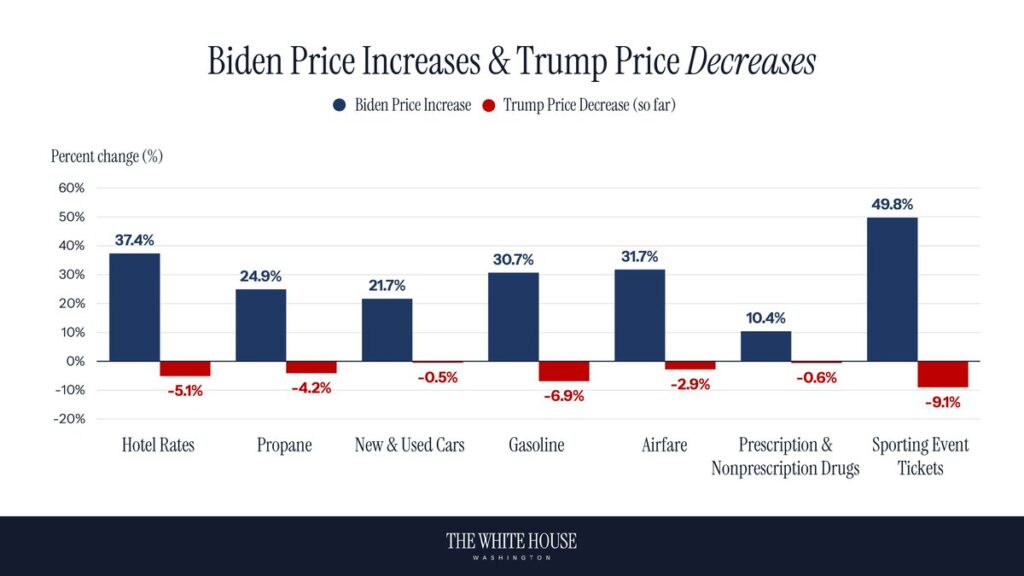

A puzzled reader might ask whether these numbers translate into daily life. They do. During the Biden years, prices rose across the board. Car prices climbed 22%. Gas rose 30%. Hotel rates jumped 37%. Airfares increased 31%. These increases were not abstract. They showed up in family budgets, eroding purchasing power month after month. Under President Trump, the direction has reversed. Prices for eggs, butter, ice cream, fresh fruit, cereal, fish, seafood, rice, pasta, and ham have all declined. The price of a Thanksgiving turkey fell nearly one-third from its Biden-era high. Everyday essentials such as toothpaste, shampoo, toilet paper, laundry detergent, and diapers have also seen substantial decreases.

Energy costs offer another clear illustration. Households that rely on propane or heating oil will pay less this winter than last. Since President Trump took office, prices for propane, kerosene, firewood, and fuel oil have all declined. Gasoline prices tell the same story. Under Biden, gas prices reached record highs even as strategic reserves were drained in a failed attempt to mask the problem. Under President Trump, gas prices have fallen to their lowest average level in 1,741 days. Americans are now on track to spend the lowest share of their disposable income on gasoline in two decades. Average prices have dipped below $3 per gallon in 39 states, below $2.75 in 24 states, and below $2.50 in seven states, with some stations falling under $2.

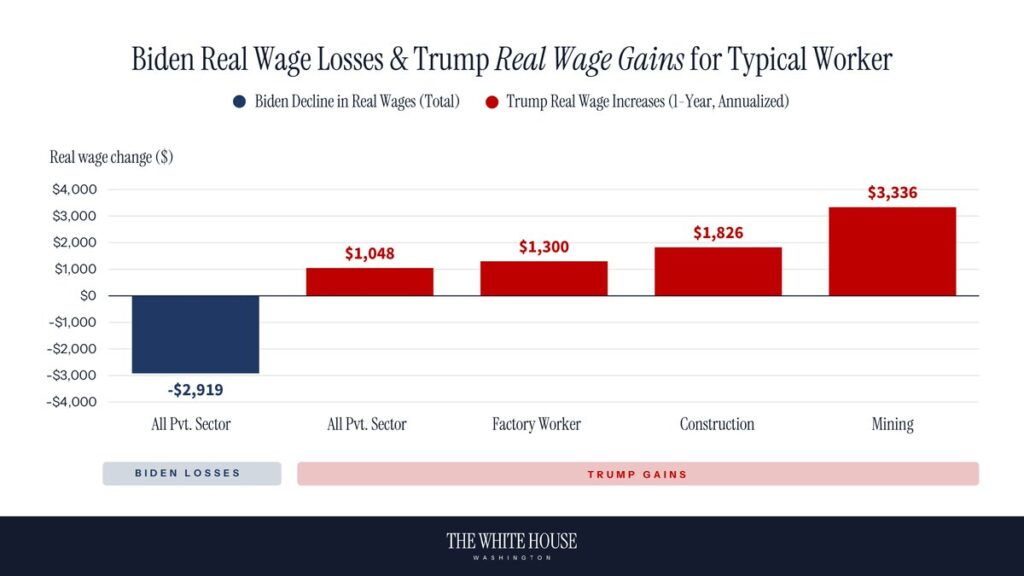

Lower prices matter, but wages matter more. Inflation can fall while households still struggle if incomes remain stagnant. That was the Biden experience. Real wages fell by nearly $3,000, a silent tax that disproportionately harmed working families. Under President Trump, the pattern has reversed. For the first time in years, wages are rising faster than inflation. After accounting for prices, real wages are on track to grow by more than $1,000 after Trump’s first full year back in office, with significantly larger gains in certain sectors. This is not accidental. It is what happens when growth replaces redistribution as the organizing principle of economic policy.

Housing affordability, long battered by a combination of inflation and open borders, is also beginning to improve. Under Biden, mortgage rates reached their highest levels in decades while rents surged. As of early December, the average 30-year fixed mortgage rate stood at 6.19%, roughly 12% lower than when President Trump took office in January. That decline translates into savings of about $3,000 per year for new homeowners. Shelter inflation is now at a four-year low, and national median rent has fallen for four consecutive months. These shifts matter because housing costs anchor household budgets. When they stabilize, everything else becomes more manageable.

Prescription drug prices provide another revealing contrast. After rising 9% under Biden, drug prices fell during President Trump’s first eight months back in office. The administration’s renewed push for a Most Favored Nation pricing framework is now producing additional reductions, with deals lowering costs for inhalers, arthritis medications, obesity drugs, infertility treatments, and more. The principle is simple. Americans should not pay more for the same medicines than patients in other developed countries. Implementing that principle required political will. President Trump supplied it.

Economic repair is not limited to prices and wages. It extends to the structure of incentives. The largest tax cuts in history are now taking effect, including No Tax on Tips, No Tax on Overtime, and No Tax on Social Security. These changes directly raise take home pay. For many households, annual income will increase by as much as $13,300, with wages rising by up to $11,600. Millions of filers are expected to receive higher tax refunds, with the average refund increasing by roughly $1,000. This is not stimulus in the Keynesian sense. It is a permanent correction that allows families to keep more of what they earn.

Deregulation has amplified these gains. President Trump’s deregulatory agenda is saving Americans an estimated $180B, or about $2,100 per family of four. One illustrative example is the rollback of Biden era appliance efficiency standards that had quietly driven up the cost of everyday household goods. Regulations often present themselves as free improvements. In reality, they impose hidden taxes. Removing them is a form of relief that does not require new spending.

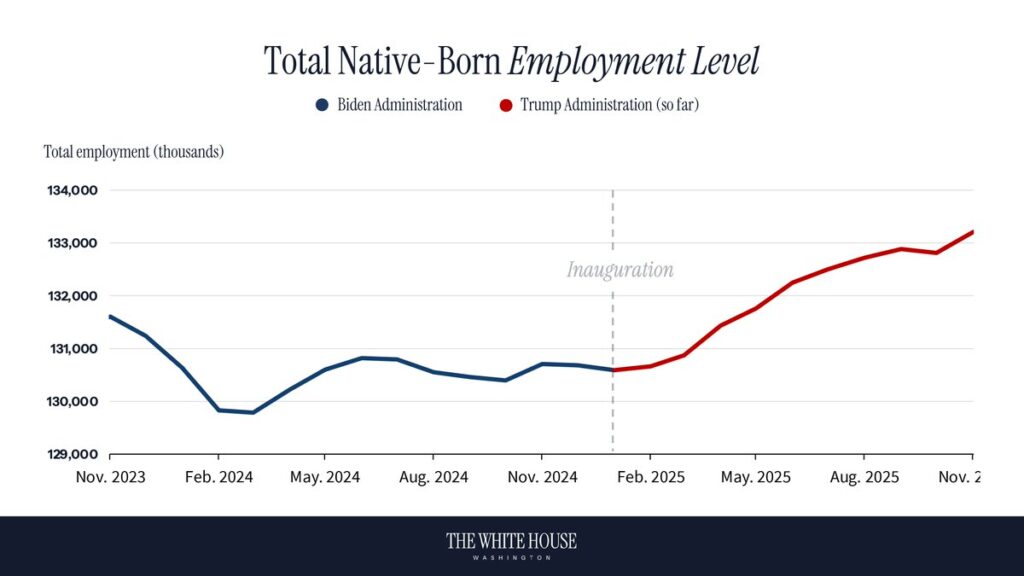

The broader economy reflects these improvements. Consumer sentiment is rising. Small business optimism is increasing. Holiday shopping and sales have reached record levels. Investment is returning home. Since President Trump took office, companies have committed trillions of dollars to US based operations, onshoring production and creating hundreds of thousands of jobs. Today, 2.7 million more American born workers are employed than when Trump began his second term, and total employment stands at an all time high.

Financial markets have responded accordingly. Since President Trump’s election, the stock market has reached 51 record highs. This is not merely a benefit for investors. Retirement accounts, pensions, and savings vehicles across the country are stronger as a result. Growth, when genuine, is widely shared.

Fiscal discipline has also returned to the conversation. Through a combination of spending restraint, interest savings, economic growth, and tariff revenue, the deficit is projected to shrink by trillions of dollars. The trade deficit has already narrowed to its smallest level since mid 2020, down more than 35% over the past year. These improvements matter because deficits are future taxes. Reducing them is an investment in long term stability.

One final example captures the administration’s governing philosophy. President Trump eliminated Biden’s aggressive fuel efficiency mandates that would have forced consumers into expensive electric vehicles regardless of suitability or cost. Those rules would have raised vehicle prices and constrained choice. Their repeal is expected to save American families $109B over the next five years. This is not hostility to innovation. It is respect for consumer judgment and economic reality.

Skeptics will say that 11 months is too short a window for judgment. In one sense, that is true. There is still work to be done, and the administration acknowledges it. But trends matter. Direction matters. After years of erosion, the fundamentals are moving in the right direction. Prices are falling. Wages are rising. Investment is returning. Confidence is rebuilding.

The deeper lesson is political as much as economic. Inflation was not inevitable. It was chosen. It followed from a worldview that treated spending as costless and production as secondary. Repair required rejecting that worldview and replacing it with one that respects markets, rewards work, and understands constraints. President Trump has done that, not rhetorically but operationally.

As the new year approaches, Americans can take stock of what has changed in just 11 months. The cost of living crisis engineered by Democrats is being unwound. The process is not complete, but it is real. For families who measure success not in press releases but in receipts, that difference is already visible.

If you enjoy my work, please subscribe: https://x.com/amuse.

Sponsored by the John Milton Freedom Foundation, a nonprofit dedicated to helping independent journalists overcome formidable challenges in today’s media landscape and bring crucial stories to you.

READ NEXT: Hunter Biden Controversy Exposes Legal Gray Area Inside Intel Community

I’m not seeing it in California. Gas is nearly $5 per gallon. Valero moved a refinery out of state and another one will be closed next year. Only four refineries in the world can make the blend of gasoline required in CA! They say it is too expensive and restrictive to do business in this state. Mr. President, please set your sights on California and Gavin Newsom.