“Self-defense liability coverage” is harder to say than “CCW insurance,” but both are difficult to understand and interpret. That whole read-the-fine print aphorism is imminently applicable here, as is the Latin phrase, Caveat Emptor. Buyer beware.

Ryan Cleckner, a firearms attorney, founder of Rocket FFL, and co-founder of Gun University, recently completed an exhaustive comparison of liability coverage programs. Among those were:

• CCW Safe

• USCCA

• Right to Bear

• Second Call

• Armed Citizens Defense League Network

• US Law Shield

law scholar, preparing to be interviewed by members of the national media.

What he found, interestingly enough, was that not only was there a wide disparity in overall quality of service, but some of the so-called “providers” actually weren’t completely familiar with the actual content and the coverage provided.

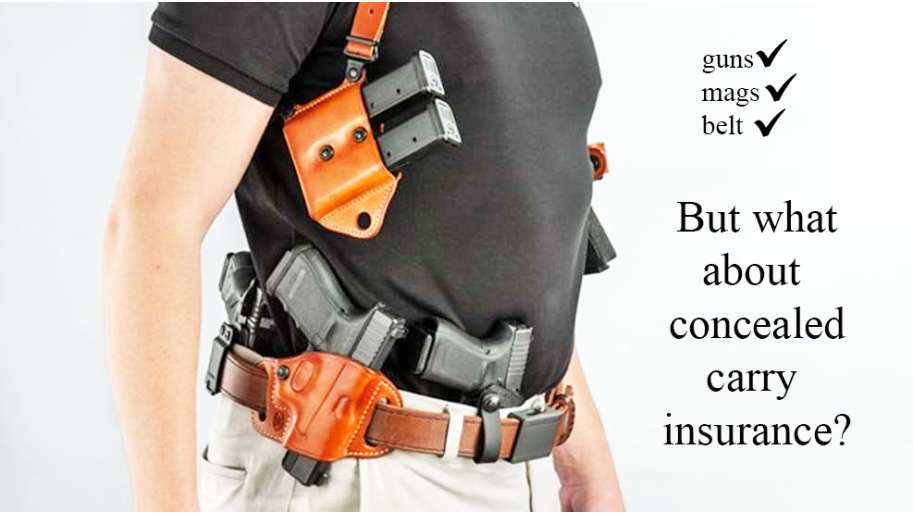

Simply explained, CCW insurance is a financial protection against the costs someone might incur if they are forced to use deadly force. Many people assume this isn’t necessary if a shooting is justified, but that has proven to be far from the case.

Cleckner, a former 75th Ranger Regiment sniper who went on to teach Constitutional Law, was intrigued by a number of high-profile cases wherein a gun owner was charged despite what seemed like objectively, reasonably, righteous circumstances. He was initially of the opinion that the cost of such liability coverage was an unnecessary expense unless someone did something unjustified and/or illegal.

Over the course of his analysis, he wound up changing his mind.

protection purchased from other companies. Some of them didn’t realize what their own plans actually

covered, and some didn’t really offer any protection at all.

Cleckner looked at several facets of each program, including (but not limited to):

- Types of legal weapons covered

- Coverage of the administrative cost

- Coverage of Private Investigator fees

- Coverage of expert witnesses

- Bail bond coverage

- Coverage of criminal defense cost

- The right to choose your own attorney

- The provision of money up front

- Availability of a daily allowance/per diem to replace lost income

- Coverage of civil defense cost

He came to several conclusions, three of which are of great significance (and at least some alarm).

- Many of these companies are “Self-Defense Liability providers”, now what you normally think of when you hear insurance: Many, if not most, “insurance” plans available for the CCW niche aren’t insurance plans at all. They’re either pre-paid legal coverage or self-defense liability plans. …

- Some of these programs are not their “own” programs. They are white-labeled plans from other providers. What they claim to cover may not always equate to what they actually cover, though that disparity might be more misunderstanding-disconnect than intentional corporate animus. …

- You should always read the fine print: and be cognizant of the fact that your “insurance” provider might not have read it themselves.

Says Cleckner,

“It’s difficult, if not impossible, to determine what self-defense liability is best for any person and their specific situation and needs…[but even] a shooting you believe was justified may still result in prosecution of a lawsuit…this may, and frequently does, occur regardless of the ultimate legal ruling on your shooting.”

Cleckner and Gun University urge everyone to read the fine print. You might incur significant financial costs even if you “win” the case; better to know ahead of time the extent of the help you can actually, contractually expect.

Read his Concealed Carry analysis HERE.

Read the original article in its entirety HERE.

This the new frontier in destroying the Second Amendment: bankrupt through litigation anyone who chooses to own, carry or, if needed, use a gun in self-defense. If it can be done with abortion – sue anyone involved with one whether it was appropriate or not – then it can be done with firearms.

Looks like neither of the top two will insure in Washington State (or two other states). I assume that’s thanks to our idiot governor, AG, and Democrat legislature. Surprised Illinois, California, Oregon and many other states aren’t excluded too.