Biden’s Parting Gift: The Collapse of the Fed’s Reverse Repo Facility

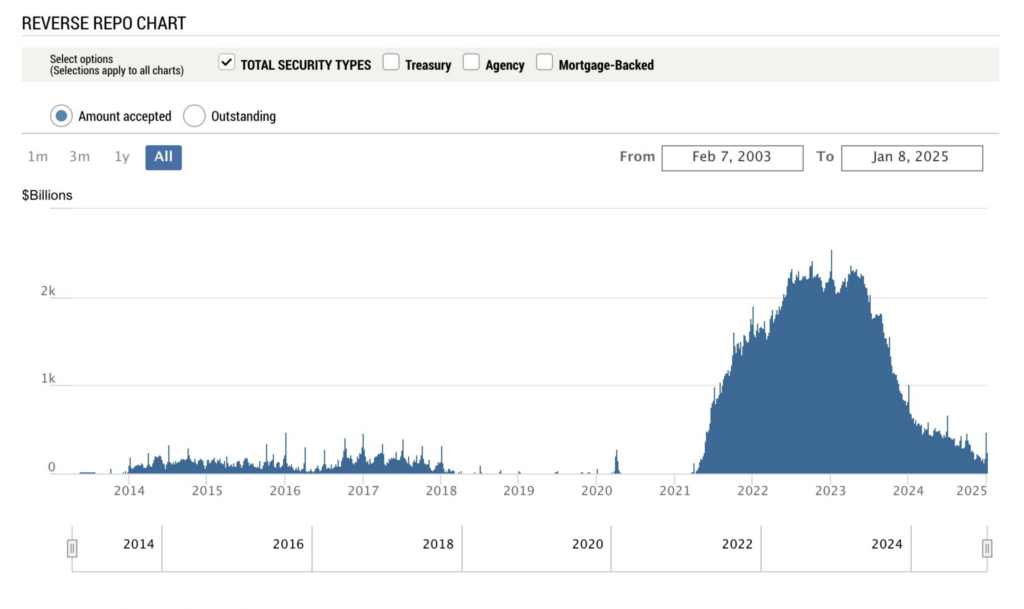

The Federal Reserve’s Reverse Repurchase Agreement (RRP) Facility has reached its lowest inventory in nearly four years. This decline signals a pivotal transition in liquidity conditions, one with far-reaching consequences for markets, institutional investors, retail investors and federal policy. The question is: How should these players respond?

To understand the significance of the decline in RRP balances, we must first recall its purpose. The RRP facility allowed money market funds, banks and other institutions to park excess cash at the Fed in exchange for Treasury securities. At its peak, the facility held over $2.6 trillion. Today, as these balances fall, liquidity is shifting into other markets. Why has this happened? First, increased Treasury bill issuance has provided alternative high-yielding assets for institutional investors, making the RRP facility less attractive. Second, the Federal Reserve’s quantitative tightening (QT) has drained liquidity from the system, further reducing RRP balances. The result is an ongoing structural shift in financial markets—one that demands strategic responses.

For financial markets, the immediate effects of shrinking RRP balances are nuanced. Increased liquidity in private money markets has softened overnight repo rates. Short-term Treasury yields remain attractive, keeping demand for T-bills high. Equities, while buoyed by available cash, face pressure from longer-term borrowing costs. Credit markets remain stable, but funding conditions are subtly shifting as banks rely more on deposits and less on excess liquidity parked at the Fed.

Looking further ahead, the continued decline of the RRP facility implies that the liquidity excesses of the pandemic era are definitively ending. This shift will likely tighten financial conditions, making corporate and consumer borrowing incrementally more expensive. It will also increase volatility in funding markets as reserves replace RRP balances as the primary liquidity buffer. Federal Reserve policy will need to adjust as policymakers calibrate balance sheet runoff to avoid unintended liquidity stress. Inflation trajectories may also be affected, as the removal of excess liquidity reduces demand-side inflationary pressures.

Institutional investors must adjust their liquidity management strategies. With RRP balances shrinking, institutions should diversify funding sources to avoid overreliance on Fed-provided liquidity. They must also adjust fixed-income portfolios to reflect a maturing QT cycle, balancing short-duration yield capture with longer-term positioning. Vigilance is necessary to identify potential dislocations in repo markets that may present opportunistic trading strategies. Additionally, institutional investors should prepare for potential increases in market volatility as liquidity conditions evolve.

Retail investors, though less directly exposed to RRP dynamics, should also take note. Maximizing yields on cash holdings while elevated interest rates persist is a prudent strategy. Adjusting asset allocation toward high-quality fixed-income instruments can take advantage of attractive yields. At the same time, reducing exposure to speculative investments that thrived on excess liquidity will help mitigate risk. Ensuring adequate liquidity buffers is also essential for weathering potential market volatility.

The Federal Reserve and Treasury will play crucial roles in managing this transition. The Fed is likely to slow or halt QT once RRP balances near exhaustion, ensuring that bank reserves remain ample. Adjustments to the interest on reserves (IOR) and RRP rate spread may also be used to steer liquidity dynamics. Meanwhile, the Treasury’s debt issuance strategy will significantly influence short-term liquidity conditions, requiring careful coordination with the Fed to prevent funding stress.

The decline in the Federal Reserve’s RRP facility marks a critical shift in financial market liquidity. While short-term stability prevails, long-term adjustments will be necessary. Institutional and retail investors must recalibrate strategies to reflect evolving liquidity conditions. Meanwhile, policymakers must ensure a smooth transition to a post-RRP financial landscape. Thoughtful navigation of this transformation will determine whether markets adapt seamlessly—or face renewed turbulence.

Sponsored by the John Milton Freedom Foundation, a nonprofit dedicated to helping independent journalists overcome formidable challenges in today’s media landscape and bring crucial stories to you.

READ NEXT: Trump Moves To End Another War: US To Finally Cut Ties

Does anyone, any fool, actually trust the Federal Reserve System? Remember it is made up of the Major banks in the US, NOT the federal government.

Read where NYC houses the gold in vaults deep underground